Executive summary

The 2025 National Retail Petroleum Site Census, researched and published by Kalibrate Canada, Inc., provides a comprehensive count and assessment of Canada’s petroleum retail outlet population. It remains a unique industry resource, offering a national view of site representation, market structure, brand and marketer relationships, outlet economics, and the evolving mix of customer offerings nationwide.

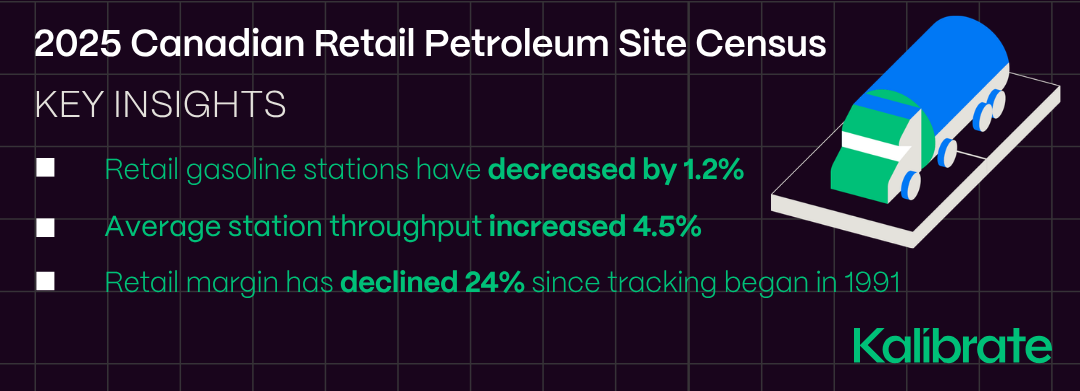

As of December 31, 2025, Canada had 11,465 retail gasoline stations, or 2.75 outlets for every 10,000 residents. This is a decline of 146 sites from the prior year and marks the lowest national site count since tracking began in the late 1980s. Even so, the long-term picture is one of relative stability compared with the steep rationalization that took place in earlier decades: after a dramatic contraction from historical peak levels, the national outlet count has hovered near today’s range for more than a decade, suggesting that the industry has moved into a more mature, slower-changing phase of network optimization.

The Canadian gas station

Our 2025 census identified 90 distinct gasoline brands and 68 fuel marketing companies operating in Canada. Although the number of consumer-facing brands has become slightly less diverse over time, the market remains structurally complex. The three largest brands—Esso, Petro-Canada, and Shell—continue to dominate the national landscape, appearing at nearly half of all sites. Yet brand visibility should not be confused with supply or pricing control. One of the most important findings in this year’s report is that the visible brand on the canopy often masks a more nuanced commercial relationship, with a growing share of sites operated by marketers who do not own the brand they sell.

The typical Canadian gas station is no longer best characterized as a site directly controlled by a refining company. In 2025, only 2,565 stations—22 percent of the national total—were price-controlled by an integrated refiner-marketer. The remaining 78 percent had pump prices set by dealers or by non-refining marketers. This is a significant structural shift from the traditional public perception of the fuel retail sector and reflects a long-running transition away from vertically integrated control toward a more distributed network of regional distributors, independent marketers, traditional non-refiner chains, and non-traditional operators.

Regional distributors and other marketers operating under branded supply agreements have become an increasingly important force in the Canadian market. In 2025, 27 fuel marketing companies incorporated another company’s brand into their networks, and these arrangements accounted for 39 percent of all stations nationwide. This evolution allows major brands to preserve or expand their consumer presence while shifting operational responsibility to marketers who can manage local networks more flexibly. For consumers, the result is continued access to trusted brands and loyalty ecosystems; for the industry, it signals a more asset-light, partnership-driven retail model.

At the same time, non-traditional petroleum marketers continue to expand their role. We identified 3,106 gasoline outlets associated with operators whose primary business is not petroleum, equivalent to 27.1 percent of Canadian sites. These networks—often tied to grocery, big box, or large-format convenience retail—have reshaped competitive dynamics in many markets through cross-promotion, loyalty integration, and high-volume business models. Their growth has been especially notable in Central and Atlantic Canada and underscores the extent to which the economics of fuel retailing are increasingly linked to broader retail ecosystems rather than to fuel sales alone.

Outlet features and offerings

The economics of the modern gasoline station help explain these structural shifts. Fuel retailing remains a high-volume, low-margin business, and the retail margin component of the pump price is relatively small. As a result, non-petroleum offerings are now central to outlet viability and competitiveness. This report shows that convenience retail, foodservice, loyalty programs, and other back-court amenities are no longer secondary features; they are increasingly core components of the Canadian gas station business model.

Convenience stores remain the most important ancillary offering. In 2025, nearly two-thirds of Canadian gasoline stations featured a convenience store larger than 500 square feet, a major shift from 2005, when large-format convenience stores were present at just over one-third of sites. The trend toward larger, more sophisticated retail footprints reflects both evolving consumer expectations and the growing need for stations to generate higher-margin non-fuel revenues. The growing presence of convenience retail specialists in the sector has accelerated this transformation and helped redefine what customers expect from a fuel stop.

Other site amenities are increasingly common. Car washes are now present at roughly one in four reporting stations, while quick-serve restaurants are available at nearly one in five. Diesel remains widely available, service bays continue their long decline, and self-serve fuelling now overwhelmingly defines the market. Together, these trends highlight a broader repositioning of the gasoline station from a single-purpose fuelling stop to a multi-service retail destination designed to capture more visits, more trip types, and more customer spend per stop.

Loyalty programs have become another important competitive lever. In 2025, 79 percent of Canadian gasoline stations offered some form of loyalty program, up from 73 percent when Kalibrate first measured this dimension in 2023. A relatively small number of major programs account for most of the market, reinforcing the advantage of larger brand and retailer ecosystems that can link fuel purchases to broader consumer reward strategies. As these programs become more sophisticated and more closely integrated with grocery, convenience, and financial partners, they are likely to play an even larger role in customer retention and share of wallet.

Average annual throughput at Canadian gasoline stations rose to 3.72 million litres in 2025, up from the prior year but still below pre-pandemic peaks. This recovery suggests resilience in the sector, yet it also highlights emerging constraints on future volume growth, including improved vehicle fuel efficiency, shifting commuting patterns, and the gradual adoption of electric vehicles. While EV charging remains a relatively modest feature within the national gasoline station network, its continued expansion signals how some operators are preparing for a more diversified transportation future. Overall, the 2025 census confirms that Canada’s fuel retail sector is becoming leaner, more operationally specialized, and more dependent on integrated retail offerings beyond fuel. For marketers, retailers, policymakers, and observers of the downstream sector, the message is clear: the Canadian gas station is no longer defined solely by what it sells at the pump, but by the broader customer proposition it can deliver on site.

For unrivalled insight into the Canadian petroleum retail market, purchase the full report.